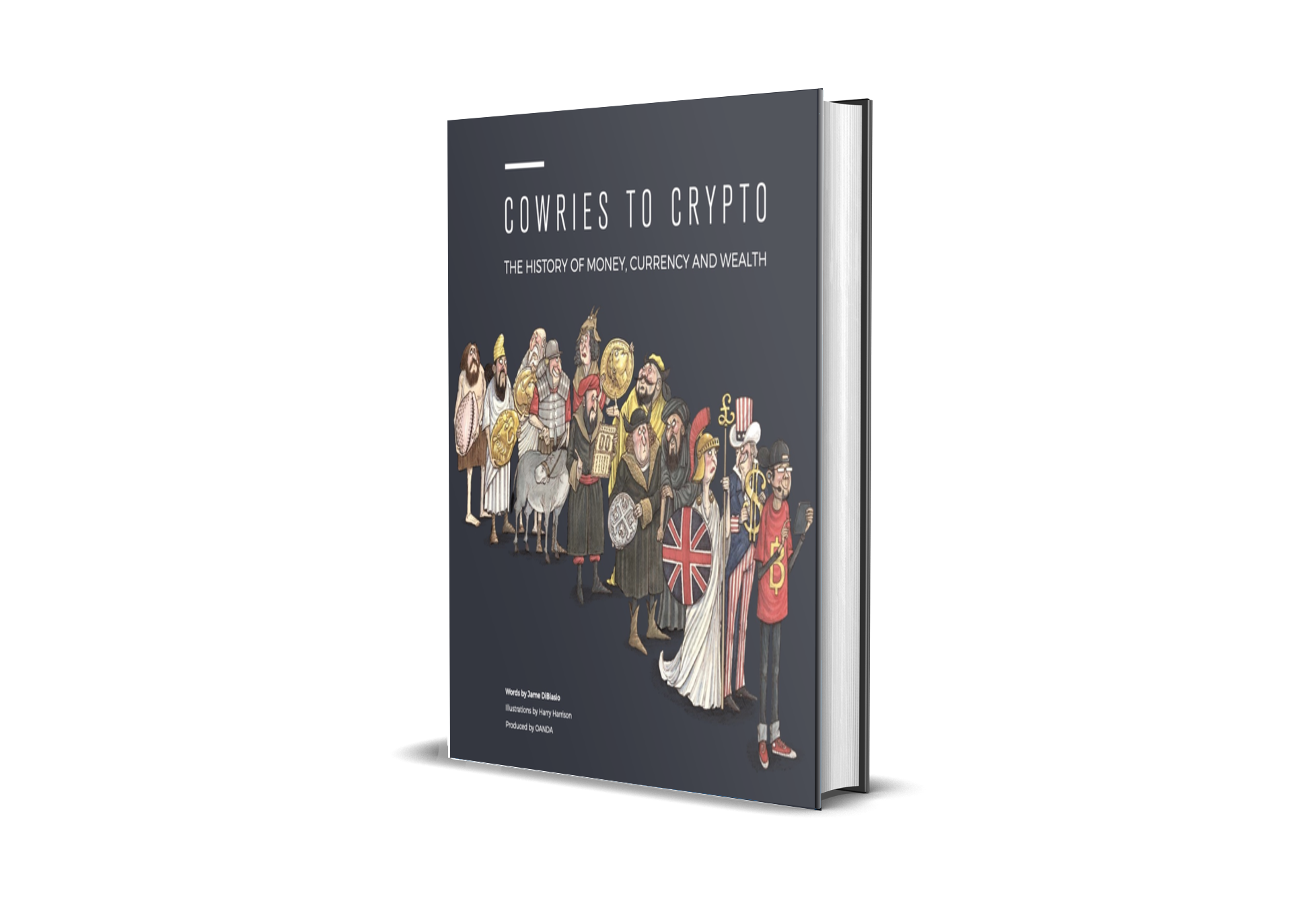

As a cashless society moves sharply into focus, a new book by Jame DiBiasio explores whether tech companies will cash in and leave banks behind

Everywhere banks look, technology companies are threatening their profits and their relevance. The world’s fintech leader is China, whose urbanites now live in a virtually cashless society. Internet companies such as Alibaba and Tencent have eaten consumer banks for lunch.

America’s big tech companies are now getting into the finance act, with Facebook famously pushing its Libra cryptocurrency for payments and Amazon and Google nibbling away at credit, insurance, and transaction banking.

At the highest echelon of finance – central banking and the currency itself – China is again leading the way with a move to a digital renminbi. The Bank of England and many other monetary authorities are also serious about following suit. This could have profound implications for commercial banks.

Much of this was speculative but now the future of banking has arrived ahead of schedule: Covid-19 has accelerated all things digital.

Is it game over for banks?

The majority of bricks-and-mortar banks do face an existential threat. A recent report by Juniper Research says 2.4 billion people already use digital banking services. That figure will jump to 3.6 billion in just four years. Banks that don’t become digital-savvy operators will miss out on that growth. Many banks will also struggle to compete with big tech. In China, the rise of “superapps” AliPay and WeChat Pay, which commingle all manner of services from gaming to food delivery to accounting, has robbed consumer banks of meaning. Citizens in China still need a bank account to access these apps, but only Alibaba and Tencent see the transaction data, leaving banks blind. It’s a future that terrifies banks in the rest of the world.

Consolidation among banks is almost certain. Already they have been closing branches, a pattern hastened by Covid-19. Bankers complain that they are fighting with one hand tied behind their backs. Fintech companies – Silicon Valley-style startups focused on tech solutions for financial services – have ™

avoided being licensed as fully-fledged financial institutions. Instead they have created layers of software that provide great user experience in areas where banks have been complacent.

Tech companies have a nose for where the banks’ margins are fattest, such as foreign-exchange fees, remittance fees, cross-border correspondent banking fees, and brokerage commissions.

And because they are not licensed, tech companies don’t have to endure banks’ endless, expensive compliance and reporting requirements.

It’s easy to move fast and break things when you don’t have to worry about being punished by regulatory bodies. However, banks in the West haven’t been able to complain too loudly – not after being bailed out in 2008 for their own recklessness. But a funny thing has happened in the past year or so. More fintechs are discovering the joys of regulation.

We may not love our banks, but we trust that the money we deposit with them will be there when we want to cash out. The same can’t be said for all-digital challenger banks or fintechs. Although some fintechs have amassed impressive user numbers, few are actually profitable, in part because most people aren’t ready to trust the startups with all of their savings.

Banks have learned to tout their advantages, which includes understanding what it means to be regulated. They understand customer protection (this hasn’t stopped them from occasionally breaching it, of course, but they understand it). They have devoted bundles of resources to compliance, risk management, and cybersecurity.

Tech companies wading into finance are discovering just how difficult it is to meet the same level of compliance and governance – even if sometimes banks treat these as box-ticking exercises. Scandals such as the Wirecard fraud, in which a German fintech payments company was found to have lied about its revenues, have highlighted the need for tech players to be scrutinised at least a bit like banks. This scepticism is likely to be extended to those that still operate successfully and legally without banking licenses, such as TransferWise.

Banks have another advantage: they have the customers, and therefore the customer data. For years, banks let this advantage go to waste because their legacy IT architecture meant they had no way of actually putting this customer data together in a meaningful way. This is why service has been so terrible. Banks are, however, starting to get the hang of how to better combine and comb through their data. Get that right, and they can begin to compete against tech arrivistes.

But tech companies are also learning from banks. Or, more accurately, they are learning how to become banks. Revolut, for example, is a fintech that started off using mobile app technology to give travellers attractive foreign-exchange rates. Today it has a banking license in Europe. In Asia-Pacific, the hottest trend is the rise of pure digital banks, with new players popping up in Australia, Hong Kong and Korea. In India, the largest mobile payments company, Paytm, now makes its revenues from a licensed banking arm.

These technology companies have realised that just being a fintech in payments, or a bank with only basic deposit services, won’t make money. What makes money is lending out depositors’ money – that is, being a bank. Conventional banks may not win the war, but they have won the argument, and the biggest ones are counter-attacking with digital strategies of their own.

However, fending off big tech will be a tougher challenge. Unlike fintech startups, the Facebooks, Googles and Amazons of this world come with vast user numbers and endless troves of data. They’re also learning how to navigate regulation. It’s hard to see how regional and community banks will survive.

We’ll still have banks, but a lot fewer of them, and those that remain may be transformed beyond recognition. My book Cowries to Crypto tells the history of money as a process of constant innovation. We are currently going through a financial transformation as seismic as any in history, with programmable money soon to displace our coins and banknotes. May the best software win.