Purpose-related investments: Liechtenstein opens up another dimension of philanthropy

John E. Kaye

- Published

- Banking & Finance, Home, Liechtenstein, Philanthropy

In July 2024, Liechtenstein further optimised its framework conditions to enable charitable foundations to make purpose-related investments in the form of impact investing and venture philanthropy. It is important to stress that tax exemption, an important quality feature of charitable foundations, will still apply. This means that charitable Liechtenstein foundations can now not only optimise the harmonisation of their funding activities and investment strategy, but can also encourage transformation processes by acting as social investors.

Charitable foundations – the ultimate risk capital?

In order to meet the major challenges of our times, charitable foundations are increasingly moving away from traditional funding activities and are redefining their role as social investors and creators of economic, social or ecological impact. After all, real change cannot be achieved by simply granting funds. It requires sustainable economic incentive mechanisms that, in the long run, lead to a new economy and society.

Charitable foundations have a special form of risk capital because, unlike companies or governments, they are not accountable to shareholders or taxpayers. They are only committed to respecting the founder’s will. However, due to their privilege of tax exemption, they are quite rightly subject to strict legal requirements, regarding both the fulfilment of their purpose and their administration. They also face the challenge of generating income through the investment of their assets while at the same time fulfilling their social responsibility.

Pursuing the foundation’s purpose holistically

Charitable foundations are generally intended to serve the common good in the areas of social welfare, science, culture, sport, environment, health or similar. The founder irrevocably cedes assets in order to dedicate them to one or more charitable goals. Traditionally, the foundation’s assets are managed professionally and the income generated is likewise used to fulfil the foundation’s purpose.

However, it has become increasingly apparent that this alone cannot suffice. In recent years, awareness of sustainable and responsible investments has grown, and consequently purpose-driven investments, such as impact investing, add an important dimension to the impact of the foundation’s activities.

Entrepreneurial forms of funding as an extension of funding activities

However, appropriate asset investments, such as impact investments, are not the only way of promoting a charitable foundation’s purpose and social investments are playing an increasingly meaningful role in their funding activities. In addition to impact investment, venture philanthropy is also developing into an important instrument. While impact investment combines the expectation of a financial return with a positive social or environmental effect, venture philanthropy is concerned primarily with maximising the impact and efficiency of the organisations it supports rather than achieving a financial return. However, both forms give rise to the question about what happens when funds or returns flow back to the charitable foundations. Since charitable foundations are not set up with a view to engaging in entrepreneurial activities, this regularly leads to the loss of tax exemption, which not only has financial repercussions, but also damages the status of the charitable foundation.

Where donating and investing are not a contradiction in terms

Liechtenstein has proactively resolved this difficulty and implemented a change in practice. In cooperation with the Association of Liechtenstein Charitable Foundations and Trusts and the Liechtenstein Institute of Professional Trustees and Fiduciaries, the authorities have expanded the relevant regulation to include purpose-related investment activities.

This clarification strengthens the country’s modern and effective foundation system. More specifically, it means that tax exemption applies not only to à-fonds-perdu contributions and services within the scope of a funding activity, but also to impact investments or entrepreneurial investments, provided that the returned funds are used as specified, namely for charitable purposes.

Those who take up this challenge and expand traditional funding models with entrepreneurial approaches must define precise goals and familiarise themselves with the complexity of impact measurement. To this end, it is advisable to work with competent partners who have practical experience in the implementation of the philanthropic approach of impact investing and can provide appropriate counselling.

Top location for charitable foundations

Liechtenstein offers ideal conditions for philanthropic engagement. In 2022, the Global Philanthropy Environment Index (GPEI) named Liechtenstein the world’s number 1 philanthropy location. The GPEI evaluates over 90 countries and economies using six key factors that comprehensively measure philanthropy: ease of operating a philanthropic organisation, tax incentives, cross-border philanthropic flows, political environment, economic environment and socio-cultural environment for philanthropy.

The GPEI stated that Liechtenstein has a highly favourable regulatory, political, economic, and socio-cultural environment for philanthropy. Tax deductions are applicable for charitable contributions to domestic philanthropic organisations as well as to organisations located in the European Economic Area (EEA) and Switzerland for both individuals and businesses. Liechtenstein’s philanthropic sector benefits from a strong tradition of philanthropic values modelled by the princely family.

Around 1,400 charitable foundations benefit from the ideal framework conditions available in Liechtenstein which offer a flexible foundation law, innovative company law, short official channels, and a high level of advisory expertise for their social or ecological commitment.

Visit Liechtenstein Finance to find out more about the financial centre Liechtenstein.

TOP STORIES

-

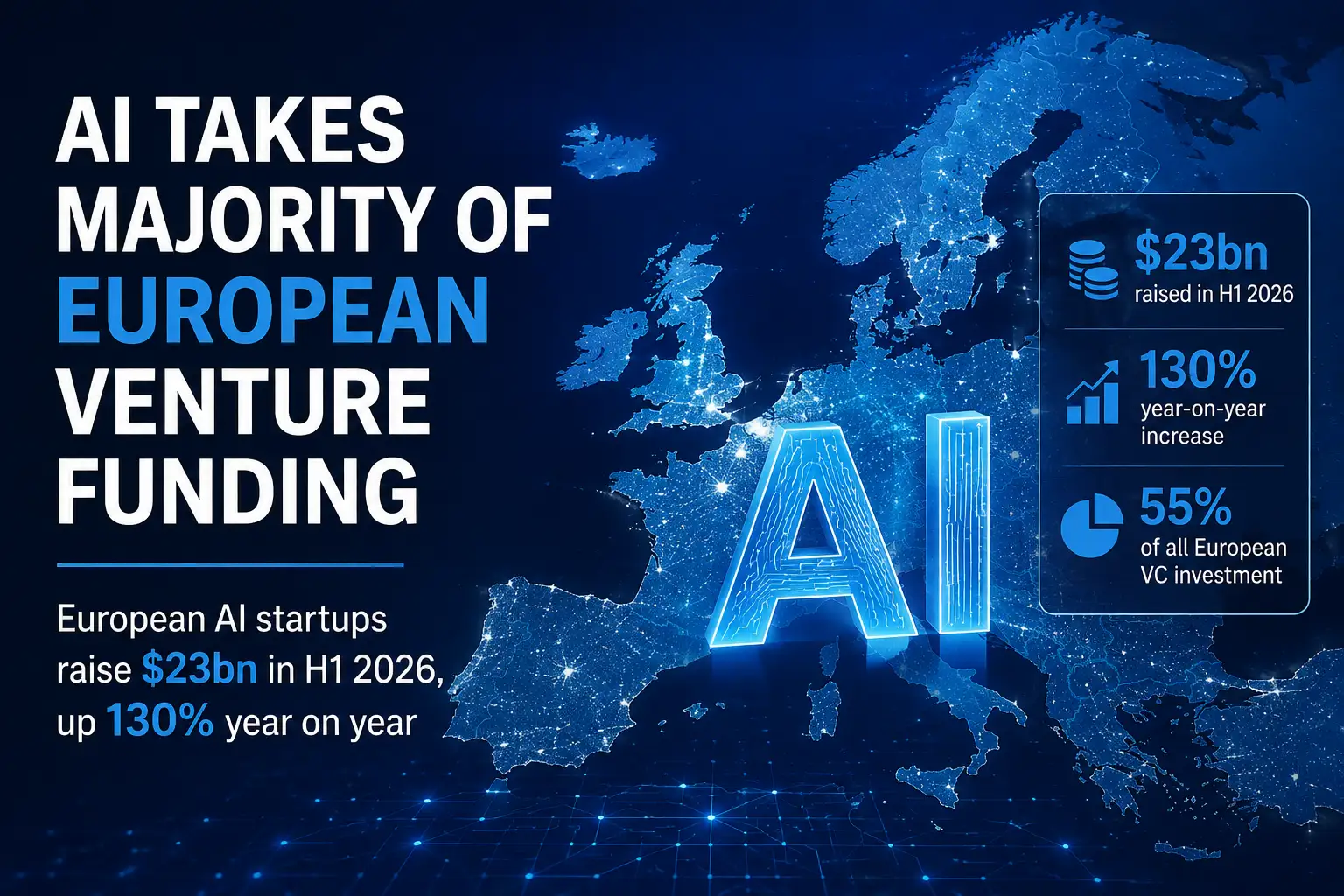

AI takes majority of European venture funding as money floods into few firms

AI takes majority of European venture funding as money floods into few firms -

RABAM raises $500,000 ahead of Series A round

RABAM raises $500,000 ahead of Series A round -

Deutsche Bank profits rise as trading business booms

-

Saab lands German frigate deal after Poland submarine order

-

BlueCrest says UK is ‘no longer serious place for business’ after £200m tax defeat

-

KPMG keeps Klaus Becker in charge of 100-country Europe, Middle East and Africa operation

-

Private banking with accountability at its core

-

Juncker and Keller-Sutter to address Zurich finance summit as banks face AI and regulation shake-up

-

Liechtenstein keeps Triple-A rating as S&P points to low debt and deep reserves

-

Liechtenstein’s stability becomes a strategic advantage in fragmented Europe

-

Germany opens door to Indian startups with Berlin launch

-

Inside Ghana’s banking revolution

-

Uzbekistan’s banking reforms signal new phase in global investment push

-

Capital without borders in a world defined by them

-

BP profits more than double as oil price surge lifts trading business

-

Cross-border structuring: what global families need to know about Liechtenstein

-

Why Liechtenstein is the launchpad for blended finance

-

Luxury SUV market forecast to top $33bn by 2036 as electric models and bigger vehicles drive demand

-

Luxury villa group Eterniti secures €30m to expand global portfolio

-

UK to slash steel import quotas as ministers target bigger share for domestic producers

-

A dram good investment: Investors turning to whisky casks and gold

-

Christian Lindner to headline Vaduz finance forum as Liechtenstein banks confront market and geopolitical strain

-

Managing cross-border risks in B2B e-commerce

-

J.P. Morgan launches first tokenised money market fund on public blockchain

-

Aberdeen agrees to take over management of £1.5bn in closed-end funds from MFS

Purpose-related investments: Liechtenstein opens up another dimension of philanthropy

John E. Kaye

- Published

- Banking & Finance, Home, Liechtenstein, Philanthropy

TOP STORIES

-

AI takes majority of European venture funding as money floods into few firms

-

RABAM raises $500,000 ahead of Series A round

-

Deutsche Bank profits rise as trading business booms

-

Saab lands German frigate deal after Poland submarine order

-

BlueCrest says UK is ‘no longer serious place for business’ after £200m tax defeat

-

KPMG keeps Klaus Becker in charge of 100-country Europe, Middle East and Africa operation

-

Private banking with accountability at its core

-

Juncker and Keller-Sutter to address Zurich finance summit as banks face AI and regulation shake-up

-

Liechtenstein keeps Triple-A rating as S&P points to low debt and deep reserves

-

Liechtenstein’s stability becomes a strategic advantage in fragmented Europe

-

Germany opens door to Indian startups with Berlin launch

-

Inside Ghana’s banking revolution

-

Uzbekistan’s banking reforms signal new phase in global investment push

-

Capital without borders in a world defined by them

-

BP profits more than double as oil price surge lifts trading business

-

Cross-border structuring: what global families need to know about Liechtenstein

-

Why Liechtenstein is the launchpad for blended finance

-

Luxury SUV market forecast to top $33bn by 2036 as electric models and bigger vehicles drive demand

-

Luxury villa group Eterniti secures €30m to expand global portfolio

-

UK to slash steel import quotas as ministers target bigger share for domestic producers

-

A dram good investment: Investors turning to whisky casks and gold

-

Christian Lindner to headline Vaduz finance forum as Liechtenstein banks confront market and geopolitical strain

-

Managing cross-border risks in B2B e-commerce

-

J.P. Morgan launches first tokenised money market fund on public blockchain

-

Aberdeen agrees to take over management of £1.5bn in closed-end funds from MFS