Oil draws back after reaching highest since March

John E. Kaye

- Published

- News, Sustainability

On Tuesday, Oil predictions slide as the market braced for reports expected to show swelling U.S. crude inventories, which pulled prices back off the highest levels since before the coronavirus pandemic slammed fuel demand.

Prices rose early, after U.S. President Donald Trump wrote a tweet late Monday regarding the trade agreement with China commenting the situation is “fully intact”. Markets had been unsettled by surprise comments from White House trade adviser Peter Navarro that the hard-won deal with China was “over”.

However, crude benchmarks declined in afternoon trade on expectations U.S. inventories will hit a record high for a third week in a row, undermining and impeding recent bullishness among investors.

Brent futures fell 45 cents, or 1.0%, to settle at $42.63 a barrel, while U.S. West Texas Intermediate (WTI) crude fell 36 cents, or 0.9%, to $40.37.

Oil extended losses in post-settlement trade after U.S. crude inventories rose by a much bigger than expected 1.7 million barrels last week, according to the American Petroleum Institute, an industry group. That compares with analysts’ expectations for a 300,000-barrel build. U.S. government data will be released on Wednesday.

Earlier, both contracts traded at their highest since prices collapsed on March 6 after the Organization of the Petroleum Exporting Countries (OPEC) and allied producers, including Russia, failed to agree on production cuts. Prices tumbled even further when the pandemic slashed fuel demand.

“It appears we ran into some technical resistance after closing the March 6 gap … and then we saw some profit taking,” said John Kilduff, partner at Again Capital LLC in New York.

U.S. crude stocks rose to 539.3 million barrels in the week to June 12, an all-time high, and are expected to have increased by 300,000 barrels in the week to June 19, according to a Reuters poll.

Additionally, weighing on crude prices, analysts said the market was unimpressed with purchasing managers reports in the United States, which showed the country’s rebound from coronavirus-depressed levels was not as sharp as in Europe.

Reported by Scott DiSavino

Sourced Reuters

For more Energy and Daily news follow The European Magazine

TOP STORIES

-

Chinese education group to buy Dublin Business School for US$127.5m

Chinese education group to buy Dublin Business School for US$127.5m -

Germany could run on full renewables by 2045, study reveals

Germany could run on full renewables by 2045, study reveals -

Marriott signs all-inclusive resort deals in Jamaica and Zanzibar

-

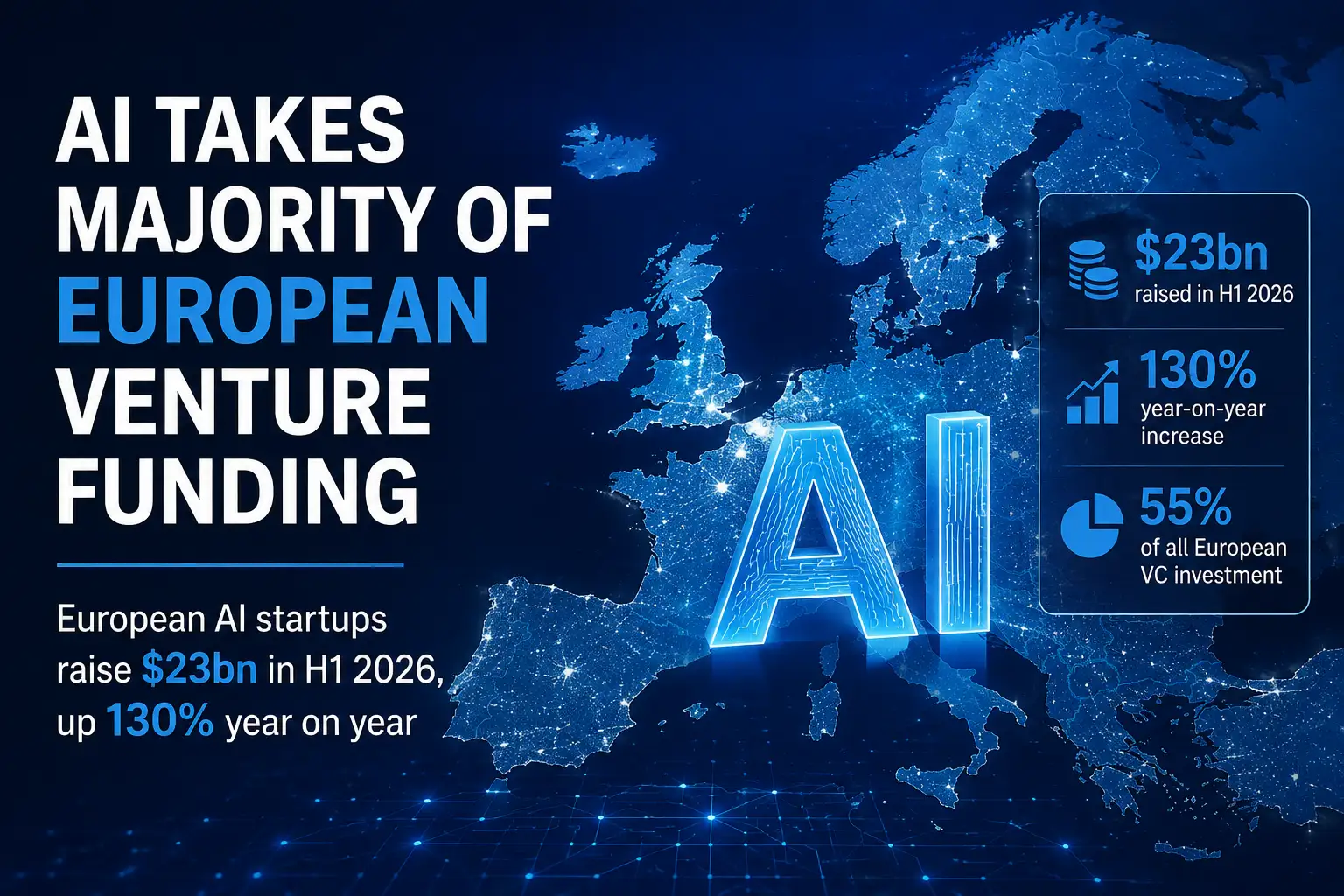

AI takes majority of European venture funding as money floods into few firms

-

Rewilding improves wellbeing and community connection, charity report says

-

RABAM raises $500,000 ahead of Series A round

-

Prologis agrees £14.3bn takeover of UK warehouse group Segro

-

Germany’s former coal heartland makes pitch as Europe’s next AI hub

-

Iran war shock hits Eurozone spending twice as hard as expected

-

Spain urges EU rules as Chinese factories move in

-

Shell earnings more than double as Middle East conflict lifts energy prices

-

Deutsche Bank profits rise as trading business booms

-

Europe’s worst wildfires in modern times could cost billions

-

The European Summer 2026 edition – out now

-

British buyers fuel Greek luxury property boom after non-dom tax change

-

New York named world’s most attractive city for tourists

-

Saab lands German frigate deal after Poland submarine order

-

Students unveil world’s first solar-powered ambulance

-

Burnham told to tackle Britain’s cyber weak spots on day one

-

Doctors using AI before health systems set the rules

-

Humanoid robots could become the next K-pop stars

-

Hormuz flashpoint keeps global shipping on high alert

-

Scientists to gather in Lisbon to tackle next pandemic threats

-

Burnham warned digital exclusion is now a national security risk

-

Masts from Kent ‘doomsday wreck’ to be cut to prevent catastrophic explosion